When it comes to acquiring a new car, the decision to lease or finance can feel like a monumental choice. Both options have their own set of advantages and drawbacks, and understanding them fully is key to making the right decision for your financial situation and lifestyle. For some, leasing offers flexibility and lower monthly payments, while others may prefer the long-term benefits and ownership that financing provides. So, how do you decide?

In this article, we'll dig deep into the differences, pros, and cons of leasing versus financing a car. We'll cover everything from the financial implications to how each impacts your lifestyle. Whether you're a first-time car buyer or someone considering a switch from leasing to financing (or vice versa), this guide will provide you with all the details you need to make an informed decision.

By the time you finish reading, you'll have a clear understanding of which option aligns best with your goals. Let’s dive into the world of car leasing and financing to help you determine which path is ideal for you!

Read also:Tips And Tricks How To Make Screen Smaller On Any Device

Table of Contents

- What Does It Mean to Lease or Finance a Car?

- How Does Leasing a Car Work?

- How Does Financing a Car Work?

- Lease vs Finance Car: Which Costs Less Upfront?

- What Are the Pros and Cons of Leasing a Car?

- What Are the Pros and Cons of Financing a Car?

- Lease vs Finance Car: Which Is More Flexible?

- How Do Mileage Limits Impact Leasing?

- Should You Lease or Finance a Car Based on Your Lifestyle?

- How Does Credit Score Affect Leasing vs Financing?

- Lease vs Finance Car: Which Offers Better Tax Benefits?

- What Happens at the End of a Lease vs Financing Term?

- Lease vs Finance Car for Business Owners

- Frequently Asked Questions

- Conclusion

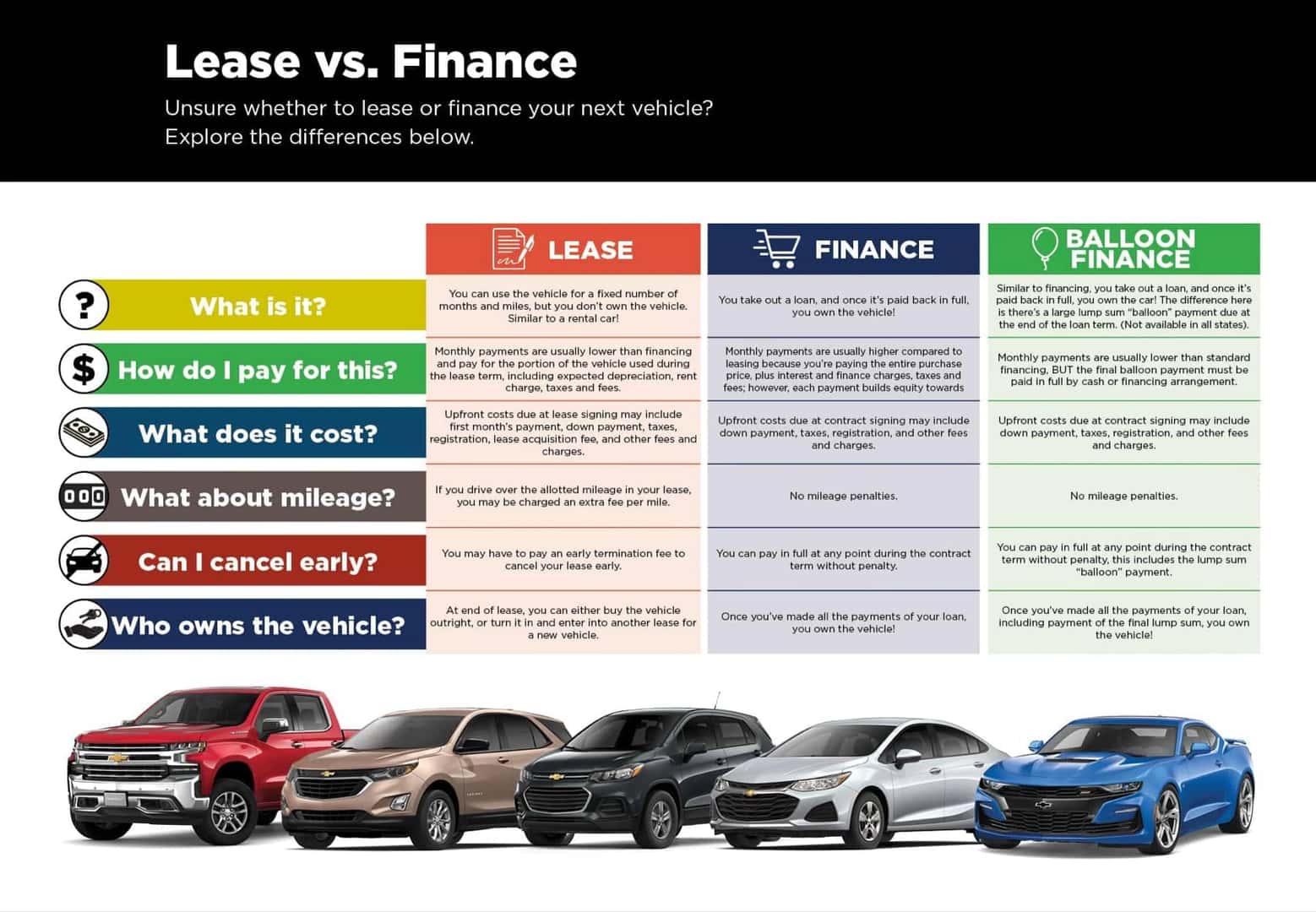

What Does It Mean to Lease or Finance a Car?

Before diving into the nuances of lease vs finance car options, let’s break down what these terms mean. Leasing a car is essentially a long-term rental agreement. You pay a monthly fee to use the car for a specific period, often two to four years. At the end of the lease, you return the car to the dealership or have the option to buy it, depending on the terms.

Financing a car, on the other hand, means taking out a loan to purchase the vehicle. You make monthly payments toward the loan, and once it’s paid off, the car is entirely yours. Where leasing focuses on temporary use, financing leads to ownership.

Both options have their merits, and your choice will depend on factors like your financial goals, driving habits, and personal preferences.

How Does Leasing a Car Work?

Leasing a car involves entering into an agreement with a dealer or leasing company. Here’s how the process typically works:

- Choose a car you want to lease.

- Negotiate the terms of the lease, including the lease duration, mileage limits, and monthly payments.

- Pay an initial down payment or security deposit (if required).

- Use the car for the agreed-upon period while adhering to mileage and wear-and-tear guidelines.

- Return the car at the end of the lease term or purchase it if the lease agreement allows.

The monthly payments for a lease are generally lower than financing. However, you don’t build equity in the car, and exceeding the mileage limit or causing excessive wear can result in extra fees.

How Does Financing a Car Work?

When you finance a car, it’s all about ownership. Here’s what to expect:

Read also:A Clarity Beyond The Depths Of Glass Darkly

- Choose a car to purchase and determine the total cost.

- Apply for an auto loan through a bank, credit union, or dealership.

- Make a down payment (usually 10%-20% of the car’s price).

- Pay off the loan in monthly installments over a set period, typically three to seven years.

- Once the loan is paid in full, you own the car outright.

While financing involves higher monthly payments compared to leasing, it gives you the benefit of ownership. You can drive the car as much as you want and customize it to your liking without worrying about lease restrictions.

Lease vs Finance Car: Which Costs Less Upfront?

One of the first factors most buyers consider is the upfront cost. Leasing a car often requires less money upfront compared to financing. Here’s why:

- Leases typically require a smaller down payment or no down payment at all.

- Monthly payments are generally lower because you’re only paying for the car’s depreciation during the lease term, not the entire cost of the vehicle.

On the other hand, financing usually involves a larger down payment to reduce the loan amount and monthly payments. While the initial cost is higher, financing allows you to build equity in the car over time.

Factors That Influence Upfront Costs

- The make and model of the car.

- Credit score and financing terms.

- Promotions or incentives offered by the dealer.

Ultimately, leasing is the more affordable option upfront, but financing offers the benefit of ownership, which could save you money in the long run.

What Are the Pros and Cons of Leasing a Car?

Leasing a car has its benefits and drawbacks. Let’s explore them:

Pros of Leasing a Car

- Lower monthly payments compared to financing.

- Access to the latest vehicle models every few years.

- Factory warranty coverage throughout the lease term.

- No long-term commitment, making it ideal for those who like to drive new cars often.

Cons of Leasing a Car

- No ownership or equity in the vehicle.

- Strict mileage limits with penalties for exceeding them.

- Potential fees for excessive wear and tear.

- Higher long-term costs if you lease repeatedly.

Leasing is a great option for those who value flexibility and lower monthly payments. However, it may not be the best choice if you’re looking for long-term financial benefits.

Frequently Asked Questions

1. Is it cheaper to lease or finance a car?

Leasing is typically cheaper upfront and has lower monthly payments, but financing is more cost-effective in the long run as you gain ownership of the vehicle.

2. What credit score do I need to lease a car?

Most leasing companies require a credit score of 700 or higher, but some may approve leases for those with scores in the 600s.

3. Can I negotiate the terms of a lease?

Yes, you can negotiate terms like monthly payments, mileage limits, and even the purchase price at the end of the lease.

4. What happens if I exceed the mileage limit on a lease?

You’ll be charged a per-mile fee, which is typically outlined in your lease agreement.

5. Can I switch from leasing to financing?

Yes, many lease agreements offer a lease-to-buy option, allowing you to finance the car at the end of the lease term.

6. Are there tax benefits to leasing a car?

For business owners, leasing a car may offer tax advantages, as lease payments can sometimes be deducted as a business expense. Consult a tax professional for details.

Conclusion

When deciding between leasing and financing a car, there’s no one-size-fits-all answer. Your choice should depend on your financial situation, lifestyle, and driving habits. Leasing offers flexibility and lower upfront costs, while financing provides the benefit of ownership and long-term savings. By weighing the pros and cons of each, you can make a decision that aligns with your goals and preferences.

If you're still unsure which option is right for you, consider speaking to a financial advisor or a car dealership representative to explore your options further. Whatever you choose, make sure it fits your budget and meets your needs.